Blog > Selling a Trust Property in Palo Alto, Los Altos, Mountain View, or Sunnyvale

Selling a Trust Property in Palo Alto, Los Altos, Mountain View, or Sunnyvale

by

Selling a home held in a trust is not simply a conventional real estate transaction with a different signature line.

The physical property may look like any other Palo Alto Eichler, Los Altos estate, Mountain View bungalow, or Sunnyvale ranch home. Behind the front door, however, sits a more complicated decision architecture: trust authority, successor-trustee documentation, beneficiary interests, title, taxes, valuation, disclosures, property preparation, personal belongings, occupancy, accounting, and the responsibility to produce a defensible result.

That is why the strongest trust-property sales begin with two parallel tracks.

The first is the fiduciary track: determining who has authority, what the trust permits, how beneficiaries should be informed, and which legal and tax professionals need to participate.

The second is the market track: determining the property’s value, condition, buyer pools, preparation strategy, pricing, disclosure package, and launch timing.

At the Boyenga Team, we bring those tracks together through a Property Nerd® process designed for trustees, successor trustees, beneficiaries, attorneys, fiduciaries, and families navigating a Silicon Valley trust sale.

The objective is not simply to place the property on the market.

It is to create a transparent, documented, market-supported transaction that respects the trustee’s responsibilities while positioning the home to achieve its strongest credible result.

The Trust-Sale Equation

A successful trust-property sale can be understood through five connected variables:

Authority + beneficiary alignment + property intelligence + market exposure + documentation

If authority is unclear, the transaction may stall.

If beneficiaries do not understand the strategy, ordinary preparation decisions can become sources of conflict.

If the property has not been properly evaluated, the trustee may spend too much, spend too little, or select the wrong pricing position.

If exposure is limited, it becomes harder to demonstrate that the market had a fair opportunity to establish value.

If the process is not documented, even a successful sale may be difficult to explain later.

Trust-property real estate is therefore both a marketing assignment and a record-building exercise.

Begin With the Trust, the Deed, and the Title Record

The first question is not, “When can we put the home on the market?”

It is, “Who currently holds legal title, who has authority to act, and what documents will the title and escrow companies require?”

A trust document may name a successor trustee, but that does not necessarily establish that a particular property was correctly transferred into the trust. The recorded deed and preliminary title report are critical.

If title is held by the trust or by the settlor as trustee, the successor trustee may be able to administer the property outside a formal probate proceeding, subject to the trust, applicable law, and the property’s specific title history. If the home was never properly transferred into the trust—or if the deed, trust, and intended ownership do not align—an attorney may need to determine whether a probate proceeding, court petition, corrective deed, or another process is required. California Courts explains that the correct transfer process depends on what the decedent owned and how it was held; some transfers require court involvement and others may not. California Courts: Guide to Property After Someone Dies

This is why the Boyenga Team prefers to involve a title officer early, not after the listing is already active.

An early preliminary title review may identify:

- The precise vesting of the property

- Recorded deeds

- Existing loans or lines of credit

- Property-tax liens

- Judgments

- Easements

- Covenants, conditions, and restrictions

- Ownership interests outside the trust

- Deceased or former trustees still appearing in title

- Documentation needed to establish successor authority

- Potential signature or recording complications

In Property Nerd language, the preliminary title report is not an escrow formality. It is the property’s legal wiring diagram.

The Certification of Trust

California law allows a trustee to present a certification of trust instead of automatically providing the entire trust instrument to establish specified trust facts. The certification can address the trust’s existence, date, acting trustees, trustee powers, revocability, tax identification number, title instructions, legal description, and—when there are multiple trustees—which signatures are required. The statute also permits certain supporting excerpts to be requested when needed to establish succession or authority. California Probate Code §18100.5

The title or escrow company may also request some combination of:

- Certification or abstract of trust

- Trust excerpts establishing authority

- Trust amendments

- Death certificate

- Affidavit of death of trustee

- Resignation, incapacity, or removal documentation

- Acceptance by successor trustee

- Tax identification information

- Identification for each acting trustee

- Supporting documentation for co-trustees

- Entity or institutional trustee authorization

The exact requirements depend on the trust, title record, escrow company, and transaction.

A trustee should not assume that the name printed on the first page of the trust is enough. Signature authority must be confirmed before the listing agreement, repair contracts, purchase agreement, and escrow documents are executed.

Determine Whether One Trustee or Multiple Trustees Must Sign

Co-trustee authority is a common source of delay.

Some trusts allow either trustee to act independently. Others require all currently acting trustees to sign. Some distinguish routine administrative decisions from the sale of real property. Amendments may change the original succession or signature provisions.

California’s certification-of-trust statute specifically contemplates identifying the acting trustees and stating whether all or fewer than all trustees must sign. California Probate Code §18100.5

This should be resolved at the beginning.

If two trustees must approve every major action, the sale calendar should include both of them. Repair proposals, price changes, disclosure documents, counteroffers, and escrow instructions should not be routed casually or at the last minute.

A technically sound transaction can still become operationally chaotic when the signature map is unclear.

The Trustee Is the Decision-Maker—but the Beneficiaries Matter

Beneficiaries do not automatically become co-sellers merely because they may ultimately receive proceeds. The trust instrument and applicable law determine authority. In many cases, the trustee is the party empowered to make decisions and execute documents.

But beneficiary communication still matters.

California law requires a trustee to administer the trust solely in the beneficiaries’ interest, deal impartially when there are multiple beneficiaries, keep beneficiaries reasonably informed, and exercise reasonable care, skill, and caution under the circumstances. California Probate Code §16002, §16003, §16040

That does not mean every beneficiary must approve every paint color or marketing decision. It does mean the process benefits from clear, consistent communication.

A strong beneficiary briefing may explain:

- The property’s estimated market position

- The condition of the home

- The proposed preparation budget

- Which improvements are recommended and why

- Which projects should be skipped

- The likely sale timeline

- The pricing strategy

- The commission and marketing structure

- Estimated closing costs

- Outstanding loans or encumbrances

- The disclosure and inspection plan

- How offers will be evaluated

- What variables could change the projected net proceeds

The purpose is to give beneficiaries visibility without creating an unworkable committee structure.

At the Boyenga Team, we often prepare written analyses, estimated net sheets, timelines, comparable-sale data, inspection summaries, proposals, and preparation recommendations that trustees can share with beneficiaries and professional advisers. The goal is to make the reasoning visible.

A fiduciary decision is easier to defend when the underlying data is organized before disagreement begins.

California Trust Notification Requirements Should Be Handled Early

When a revocable trust becomes irrevocable because of a settlor’s death, or when specified trustee changes occur, California Probate Code §16061.7 can require formal notification to beneficiaries and heirs. The statute generally calls for notice within 60 days after the triggering event or after the trustee becomes aware of an entitled person; the notice also contains information about the trust and a warning concerning the period for bringing a trust contest. California Probate Code §16061.7

This is attorney territory.

The real estate team should not draft legal trust notices or determine who must receive them. But the listing timeline should account for the trust-administration work being performed by counsel.

An aggressive market date should not be selected without understanding whether the trustee’s succession, notifications, authority, and beneficiary communications are sufficiently organized.

Build the Professional Team Before Building the Listing

A trust-property sale may involve several specialists:

- Trust or estate attorney

- CPA or tax adviser

- Title officer

- Escrow officer

- Appraiser

- Real estate team

- Property inspector

- Roof, pest, sewer, chimney, pool, or other specialists

- Contractor, painter, landscaper, and stager

- Property manager or landlord-tenant counsel if occupied

- Financial adviser

- Professional fiduciary

- Estate-sale or personal-property specialist

The real estate agent should coordinate the property and market process, but should not attempt to replace legal, tax, appraisal, or fiduciary advice.

The most efficient trust sales are not the ones with the fewest professionals. They are the ones in which each professional addresses the correct question early enough to prevent a later problem.

Establish Two Different Values: Date-of-Death Value and Market Value

Trustees often hear the word “value” used as though it means one thing. In a trust sale, it may refer to two distinct analyses.

Date-of-Death Valuation

A qualified appraisal may be needed to establish the property’s fair market value as of the decedent’s date of death or another applicable valuation date. This may be relevant to tax basis, trust accounting, estate administration, or reporting.

The IRS states that inherited property’s basis is generally its fair market value on the date of death, subject to exceptions and special rules. Joint ownership, community property, prior gifts, depreciation, alternate valuation, and the trust’s tax classification can change the analysis. IRS Publication 559: Basis of Inherited Property

This retrospective appraisal is not necessarily the same as the property’s current listing value.

Current Market Valuation

The listing team evaluates what the property could command in the current market after considering:

- Recent comparable sales

- Pending transactions

- Active competition

- Condition

- Lot utility

- Architecture

- Street position

- School information

- Preparation level

- Buyer demand

- Search-price thresholds

- Seasonal timing

- Current financing conditions

- Likely offer structure

A date-of-death appraisal answers a historical valuation question. A current comparative market analysis answers a present-day marketing question.

Trustees should avoid substituting one for the other.

Separate Personal Property From Real Property

A trust-property sale often begins with a house full of belongings, records, family photographs, art, furniture, tools, jewelry, documents, and items carrying emotional value.

The real estate preparation process should not begin with a dumpster.

First determine:

- Which items are specifically distributed by the trust

- Which items beneficiaries wish to retain

- Whether any property requires appraisal

- Whether there are valuables, documents, firearms, medication, or sensitive records

- Whether an estate sale or auction is appropriate

- Which items belong to an occupant or tenant

- Which fixtures are part of the real property

- Which items may be excluded from the sale

- Who has authority to approve removal or disposal

Photographic inventory can be useful, particularly when beneficiaries live in different locations. Valuable or disputed items should be handled according to the trust, legal advice, and a documented process.

Only after personal-property decisions are substantially complete should the home move into full preparation.

This protects the family, the trustee, and the sale timeline.

Determine Whether the Property Is Vacant, Owner-Occupied, Tenant-Occupied, or Occupied by a Beneficiary

Occupancy changes the entire project.

A vacant home can usually be inspected, repaired, cleaned, staged, and shown on a controlled schedule.

An owner-occupied home may require sensitivity, especially when the occupant is a surviving settlor or trustee.

A tenant-occupied property introduces lease terms, deposits, access requirements, relocation questions, rent history, local and state housing rules, and potential limits on the seller’s timeline.

A beneficiary or family member living in the home can create another layer of complexity. Their rights, expectations, personal property, move-out plan, and communication with the trustee need to be addressed carefully.

Do not treat an occupant as a preparation obstacle to be “worked around.” Establish the legal and practical occupancy plan before contractors, stagers, or photographers are scheduled.

When the property is tenant-occupied or possession is disputed, the trustee should consult qualified landlord-tenant counsel before giving notices, changing access, making promises to buyers, or selecting a market date.

The Trust-Property Preparation Decision

Once authority, title, personal property, occupancy, and valuation are understood, the trustee can choose among three broad market-preparation strategies.

Strategy One: Sell Substantially As-Is

An as-is strategy may be appropriate when the home needs extensive renovation, the trust lacks available cash, the trustee prioritizes speed, beneficiaries prefer not to fund improvements, or construction risk outweighs the probable return.

As-is does not mean invisible, dirty, undocumented, or poorly marketed.

Even an as-is property may benefit from:

- Personal-property removal

- Deep cleaning

- Yard cleanup

- Window washing

- Improved lighting

- Professional photography

- Floor plans

- Pre-sale inspections

- Organized disclosures

- Accurate architectural and lot storytelling

- Careful staging or selective virtual presentation

- Multiple-buyer-pool marketing

The market should be allowed to see the property’s potential without being distracted by preventable clutter.

Strategy Two: Selective Market Preparation

For many Silicon Valley trust properties, this is the highest-efficiency strategy.

Selective preparation concentrates on work that improves buyer confidence, photography, functionality, and perceived care without triggering a major renovation.

It may include:

- Interior and exterior paint

- Flooring repair or replacement

- Lighting updates

- Hardware

- Cabinet refinishing

- Bathroom detailing

- Minor plumbing and electrical repairs

- Roof or gutter servicing

- Landscaping

- Hardscape cleaning

- Window cleaning

- Deep cleaning

- Professional staging

The Property Nerd question is not whether each improvement looks better. It is whether it is likely to improve the home’s market position enough to justify its cost, time, and execution risk.

Strategy Three: More Extensive Transformation

A larger preparation program may make sense when the condition gap between the property and its competitive set is substantial, the work can be completed predictably, the budget is available, and the likely buyer response supports the investment.

This might include flooring throughout, kitchen counters, cabinet refinishing, bathroom refreshes, lighting packages, exterior restoration, or a more comprehensive landscape plan.

Major structural remodeling immediately before a trust sale is usually a more complicated proposition. Permits, design, material lead times, change orders, concealed conditions, and beneficiary concerns can significantly increase risk.

The ideal trust-property preparation plan is not the one that spends the most. It is the one that creates the strongest relationship between investment and market response.

Document Every Preparation Dollar

Trustees should maintain a clean record of preparation expenses.

The project file may include:

- Vendor proposals

- Signed approvals

- Invoices

- Receipts

- Proof of payment

- Before-and-after photographs

- Permits

- Warranties

- Inspection reports

- Repair documentation

- Credits or reimbursements

- Staging contracts

- Landscaping records

- Cleaning and hauling expenses

When multiple beneficiaries are involved, an expense ledger can prevent confusion about where money was spent and why.

The Boyenga Team can organize the property-preparation side of this record, while the trustee and advisers determine the appropriate trust-accounting and tax treatment.

Disclosures in a California Trust Sale

Trust sales are sometimes described casually as “exempt sales.” That shorthand can be dangerous.

Certain fiduciary transfers in the administration of a decedent’s estate or trust may be exempt from specific statutory disclosure requirements, depending on the facts—including whether the trustee was a former owner. The California Department of Real Estate’s disclosure guide discusses this exemption while also emphasizing that sellers and agents must make disclosures necessary to avoid fraud, misrepresentation, or deceit. California DRE: Disclosures in Real Property Transactions

The practical rule is simple:

An exemption from a particular form is not permission to conceal known material facts.

The trustee may have limited personal knowledge, especially if they never occupied the property. That lack of knowledge should be stated accurately. It should not be converted into unsupported answers.

The disclosure strategy may draw from:

- Trustee or exempt-seller disclosures

- Agent visual inspection

- General property inspection

- Pest inspection

- Roof report

- Sewer lateral report

- Chimney inspection

- Pool inspection

- Foundation or drainage evaluation

- Permit records

- Repair invoices

- Prior reports

- Insurance claims known to the trustee

- Tenant or property-manager information

- Correspondence concerning defects or disputes

- Natural hazard disclosures

- Preliminary title information

Pre-sale inspections can be particularly useful in trust sales because they replace some of the missing owner history with professional observations.

They do not eliminate every unknown, and they are not warranties. They give buyers a more organized basis for evaluating condition.

Tax Basis Is Not the Same as Property-Tax Assessment

Trustees and beneficiaries frequently confuse three different concepts:

- Income-tax basis

- Current market value

- Property-tax assessed value

They are not interchangeable.

Income-Tax Basis

For inherited property, federal basis is generally tied to fair market value at death, subject to important exceptions and ownership-specific rules. IRS Publication 559

The trustee should consult a CPA or estate-tax professional regarding basis, capital improvements, selling expenses, depreciation, community-property rules, and the identity of the taxpayer reporting the transaction.

California Real Estate Withholding

California generally requires real estate withholding unless an exemption or alternative applies. The 2026 Form 593 instructions specifically address trusts, including the tax identification information used after a grantor trust becomes irrevocable at death. They also explain that an exemption from withholding does not remove the obligation to file a return and pay any tax ultimately due. California FTB: 2026 Form 593 Instructions

Trustees should coordinate with escrow and their tax adviser before closing so the form reflects the correct trust name, tax classification, identification number, exemption, estimated gain, and reporting party.

Proposition 19 and Property-Tax Reassessment

Proposition 19 substantially changed California’s parent-child and grandparent-grandchild property-tax exclusions. For qualifying intergenerational transfers, the inherited property generally must have been the transferor’s principal residence and become the transferee’s principal residence, with a value limitation and filing requirements. The exclusion for other inherited real property was eliminated under the current framework. California State Board of Equalization: Proposition 19

If the trust plans to sell the property to a third party, the practical effect may differ from a beneficiary retaining and occupying it. Trustees and beneficiaries should obtain property-tax and legal advice before deciding whether to distribute, retain, occupy, or sell.

A real estate marketing decision should not be made without understanding the tax consequences of the ownership decision surrounding it.

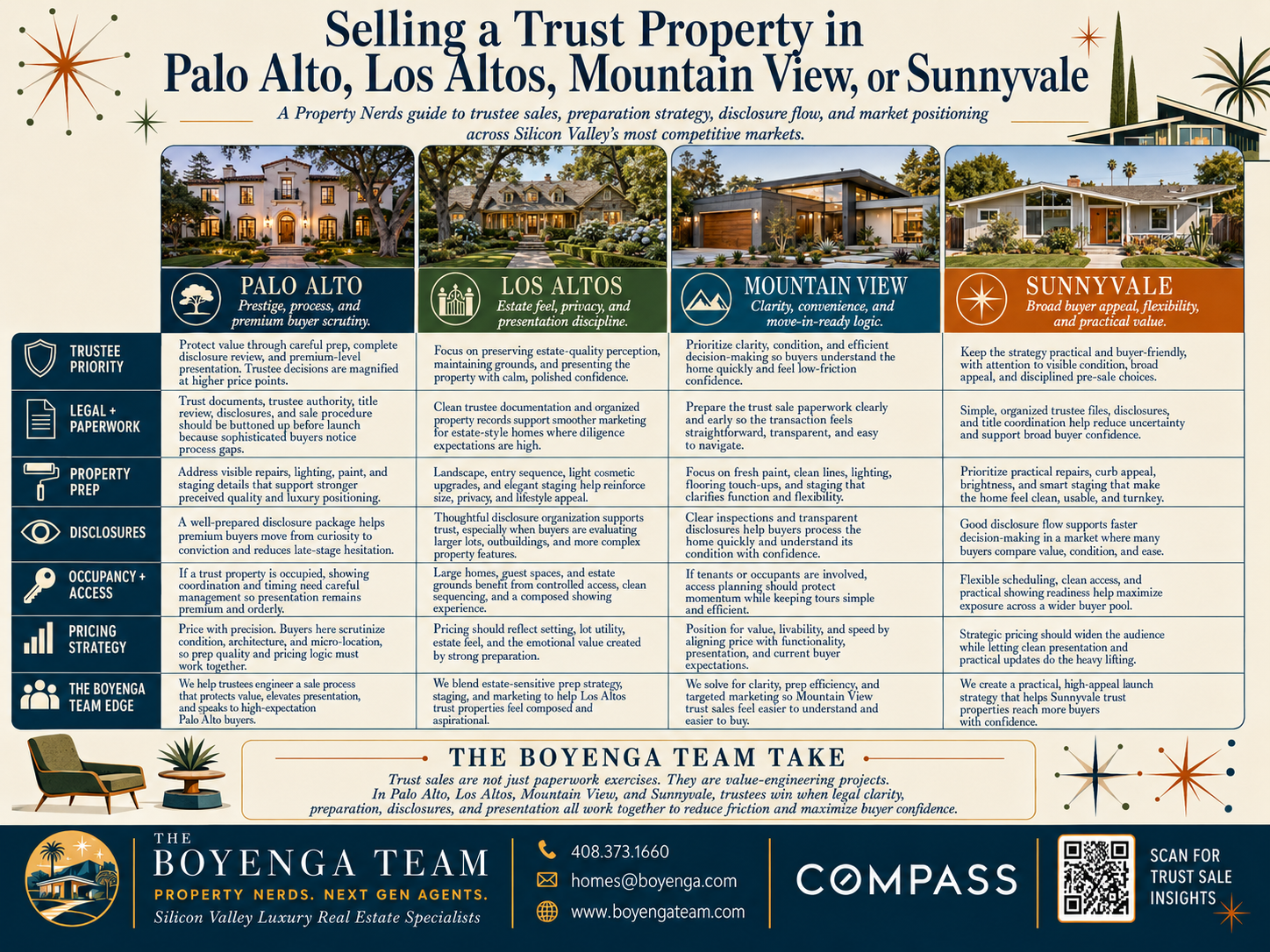

Preparing a Palo Alto Trust Property for Sale

Palo Alto trust properties frequently involve homes held for decades. Some have undergone several remodels; others retain original architecture and systems. Permit history, additions, converted spaces, mature trees, drainage, foundations, roofs, and property-line conditions may require careful review.

The preparation plan should be architecture-specific.

A Craftsman, Spanish-style home, contemporary rebuild, ranch residence, and Eichler should not receive the same cosmetic treatment. Original wood, millwork, ceiling details, masonry, globe lighting, mahogany paneling, and post-and-beam elements may contribute to value.

Palo Alto buyers may also evaluate the property through neighborhood identity, applicable school information, Stanford proximity, commute patterns, lot utility, and future flexibility. The marketing should give each of those buyer pools a credible path into the listing.

When a home has been held for many years, the trustee may not know which work was permitted or when a system was replaced. That is a reason to investigate and disclose carefully—not to guess.

For Eichler and modernist trust properties, the Boyenga Team maintains specialized resources through Palo Alto Eichler Home, Eichler Homes for Sale, and Bay Area Eichler Homes.

Preparing a Los Altos Trust Property for Sale

Los Altos trust properties often derive significant value from land, privacy, mature landscaping, interior scale, and indoor-outdoor relationships.

A trustee should be cautious about evaluating the property only through its existing finishes. A dated home on a strong lot may attract remodelers, end users, architectural buyers, or buyers considering a more substantial transformation. The market strategy should expose the property to each credible pool.

Large properties also create more due-diligence variables:

- Survey and boundary information

- Easements

- Private roads

- Drainage

- Retaining walls

- Trees

- Pools

- Wells or septic systems where applicable

- Detached structures

- Additions

- Guest spaces

- Permit history

- Landscaping and irrigation

- Development or expansion questions

Marketing should distinguish verified facts from possibilities. An unverified assumption about an ADU, addition, lot split, or redevelopment scenario should never be presented as a certainty.

Staging and photography should explain the entire property. A Los Altos trust sale can be undermarketed when the campaign photographs only the house and fails to communicate the grounds, outdoor rooms, privacy, or scale.

Modernist-property resources are also available at Los Altos Eichler Home and MidMod Homes.

Preparing a Mountain View Trust Property for Sale

Mountain View contains a wide range of housing types, including downtown bungalows, ranch homes, Eichlers, condominiums, townhomes, and newer construction.

The competitive set must be defined carefully. A Monta Loma Eichler should not be valued as a generic ranch house. A downtown bungalow may derive substantial value from its setting and walkability even if the interior is smaller. A Waverly Park residence may compete through lot utility, floor plan, and neighborhood character.

Trustees should evaluate how efficiently the property’s square footage is being communicated. Smaller homes are especially sensitive to clutter, oversized furniture, inconsistent flooring, dark paint, and undefined rooms.

Strategic staging can demonstrate that a compact property supports living, dining, work, guests, and outdoor use without feeling overfilled.

Mountain View buyers may also compare the home with Palo Alto, Sunnyvale, Los Altos, or Santa Clara. Comparative marketing can create additional buyer pools by explaining the property’s balance of location, architecture, space, condition, and price.

The Boyenga Team’s specialized modernist coverage includes Mountain View Eichler Home.

Preparing a Sunnyvale Trust Property for Sale

Sunnyvale trust sales often involve long-held ranch homes, Eichlers, and properties with meaningful lot value.

The city’s housing demand is influenced by a complex intersection of neighborhood identity, school-district and attendance-boundary information, proximity to Apple, Google, Nvidia, LinkedIn, Caltrain, and major commute corridors.

A trust property may therefore appeal to several different audiences:

- Buyers prioritizing location and commute

- Buyers focused on applicable school information

- Eichler and mid-century modern buyers

- Buyers seeking a larger lot

- Buyers looking for a turnkey home

- Buyers willing to make cosmetic improvements

- Buyers comparing Sunnyvale with Cupertino or Mountain View

- Buyers seeking office or flexible-use space

The listing should not flatten these advantages into generic language.

A Cherry Chase-area ranch, Fairbrae Eichler, Birdland home, downtown property, or Lakewood residence may require a different preparation, pricing, and content strategy.

For Sunnyvale Eichler homes, see Sunnyvale Eichler Home and Bay Area Eichler Homes.

Eichler Trust Properties Require Architectural Fluency

An Eichler held in trust may retain original elements that are increasingly difficult to reproduce. Those features should be evaluated before contractors begin making generic updates.

Potentially significant elements include:

- Post-and-beam structure

- Atrium configuration

- Floor-to-ceiling glass

- Radiant-heated slab

- Original globe lighting

- Mahogany paneling

- Ceiling decking

- Original cabinetry

- Lauan doors

- Vertical-groove siding

- Indoor-outdoor sightlines

Not everything original is valuable in its current condition, and thoughtful modernization can improve functionality. But an uninformed renovation may permanently remove the characteristics that distinguish the home from conventional inventory.

The correct question is not, “How do we make this Eichler look like a new house?”

It is, “How do we present this Eichler as the most compelling version of its architectural identity?”

The Boyenga Team’s broader Eichler network includes EichlerHomesForSale.com, JoeEichler.com, CupertinoEichlerHome.com, SanJoseEichlerHome.com, SanMateoEichlerHomes.com, and FosterCityEichlerHome.com.

Create a Pricing Record the Trustee Can Explain

Trust-property pricing should be supported by more than a neighborhood average or a single price-per-square-foot calculation.

The analysis should show:

- The most relevant closed sales

- Pending sales where reliable information is available

- Active competition

- Withdrawn, expired, or reduced listings

- Differences in square footage

- Lot-size and lot-utility adjustments

- Condition

- Architecture

- School information

- Street position

- Remodel quality

- Buyer search thresholds

- Market timing

- Preparation level

- Expected offer structure

Price per square foot is useful, but it is not a complete valuation model. Larger homes frequently trade at a different price-per-square-foot level than smaller homes. A unique architectural property may not track conventional inventory. A superior lot can materially change value even when the existing house is dated.

A defensible pricing record explains why certain comparable sales deserve more weight than others.

It also distinguishes the likely market-value range from the strategic list price. Those are related, but not always identical.

Expose the Property to Multiple Buyer Pools

A trustee is generally better served by broad, credible market exposure than by a narrow campaign built around a single buyer profile.

The Boyenga Team creates multiple digital doorways into a listing through:

- MLS and portal exposure

- Property-specific websites

- Professional photography

- Cinematic video

- Floor plans

- Aerial imagery

- Architectural marketing

- Neighborhood guides

- City-comparison content

- Employer-proximity content

- Eichler and mid-century websites

- Social media

- Email campaigns

- Agent-to-agent outreach

- Relocation marketing

- Open homes and private showings

A Palo Alto trust property may reach architecture-first buyers, Stanford-area buyers, neighborhood-focused buyers, and buyers comparing Mountain View or Los Altos.

A Los Altos property may reach luxury buyers, land-focused buyers, remodelers, architectural buyers, and buyers seeking indoor-outdoor living.

A Mountain View home may appeal through walkability, Google proximity, architecture, Caltrain access, or comparative value.

A Sunnyvale listing may intersect with Apple-area, Nvidia-area, school-information, Eichler, lot-value, and turnkey buyer searches.

The property needs one coherent identity—but it can have several authentic reasons to be purchased.

Evaluate Offers Like a Fiduciary, Not Merely a Seller

The highest stated price is not always the strongest offer.

A trustee should evaluate the entire risk-adjusted package:

- Price

- Financing

- Down payment

- Deposit

- Loan contingency

- Appraisal contingency

- Property contingency

- Disclosure review

- Close of escrow

- Possession

- Credits

- Seller-paid costs

- Requested personal property

- Assignment rights

- Sale-of-buyer’s-property conditions

- Evidence of funds

- Lender quality

- Buyer-agent communication

- Probability of performance

In Property Nerd terms:

Offer value = price − execution risk − concession exposure − timing cost

A slightly lower offer with strong financing and cleaner terms may produce a more reliable net result than a higher offer carrying substantial appraisal, loan, sale, or renegotiation risk.

The analysis should be documented and presented in a way that the trustee can understand, share with counsel when appropriate, and explain to beneficiaries.

Closing the Trust Sale

Before closing, the trustee, escrow officer, title company, CPA, and attorney may need to coordinate:

- Final title documents

- Trustee signatures

- Loan payoffs

- Property-tax adjustments

- Transfer taxes and recording charges

- California Form 593

- Trust or estate tax identification number

- Seller proceeds instructions

- Repair invoices

- Brokerage compensation

- Beneficiary or trust accounting records

- Keys, remotes, warranties, and possession

- Post-closing reserves

- Final utility handling

- Insurance cancellation timing

The sale proceeds generally belong to the trust or appropriate selling entity—not automatically to the beneficiaries at the moment of closing. Distribution timing, reserves, debts, taxes, fees, and accounting should be determined by the trustee and professional advisers.

The real estate closing is an important milestone, but it may not be the final step in the trust administration.

Common Trust-Property Sale Mistakes

Listing Before Confirming Authority

A signed listing agreement is not a substitute for reviewing title, the trust, trustee succession, and signature requirements.

Allowing Informal Family Consensus to Replace Trustee Process

Beneficiary input is valuable, but unclear decision authority can create delay and inconsistent instructions.

Using a Date-of-Death Appraisal as the Current List Price

A historical tax valuation and a current market-positioning analysis answer different questions.

Throwing Away Personal Property Too Quickly

Items should be reviewed, documented, and distributed or disposed of according to the trust and professional advice.

Assuming “Exempt Sale” Means “No Disclosures”

Exemption from a particular statutory form does not authorize concealment of known material facts.

Renovating Without Running the Prep Math

The trust may spend heavily on improvements buyers do not reward—or skip modest work that could materially improve presentation.

Underexposing an Architectural Property

An Eichler, modernist home, historic residence, or design-sensitive property should be marketed to specialized audiences as well as the general market.

Choosing an Offer by Price Alone

Financing, contingencies, appraisal exposure, credits, closing timing, and probability of performance all affect the trust’s final outcome.

Failing to Preserve the Decision Record

Trustees should maintain proposals, valuations, reports, invoices, communications, and offer analyses.

The Boyenga Team’s Trust-Property Process

Eric and Janelle Boyenga of the Boyenga Team at Compass combine fiduciary-sensitive communication with Silicon Valley market analysis, property preparation, staging, architectural expertise, disclosure organization, pricing, multiple-buyer-pool marketing, and transaction management.

Known as the Property Nerds®, they help trustees convert a complicated property into an organized market process.

The Boyenga Team can assist with:

- Preliminary property and title coordination

- Trustee and beneficiary presentations

- Comparative market analysis

- Date-of-death appraiser coordination

- Estimated seller net sheets

- Property-condition review

- Pre-sale inspection strategy

- Preparation budgets

- Vendor coordination

- Staging

- Architectural positioning

- Eichler-specific marketing

- Disclosure organization

- Multiple-buyer-pool strategy

- Offer comparison

- Escrow coordination

- Consistent progress reporting

Explore additional resources at BoyengaTeam.com, Boyenga.com, BoyengaRealEstateTeam.com, SiliconValleyRealEstate.com, and BoyengaGroup.com.

If you are serving as trustee, successor trustee, professional fiduciary, attorney, or family representative for a property in Palo Alto, Los Altos, Mountain View, Sunnyvale, or another Silicon Valley community, contact Eric and Janelle Boyenga for a confidential property and market consultation.

Let the Boyenga Team solve the trust-property equation—and engineer a clear path from responsibility to resolution.

This article provides general real estate information and is not legal, tax, accounting, appraisal, or fiduciary advice. Trusts, title histories, tax circumstances, occupancy, and beneficiary rights differ. Trustees should consult qualified California legal and tax professionals regarding their specific responsibilities.