- Buy

- Sell

- Home Value

- Areas

- Los Altos

- Palo Alto

- Evergreen Park, Palo Alto

- College Terrace

- Charleston Meadows | Boyenga Team

- Charleston Gardens

- Crescent Park

- Downtown North

- Fairmeadow

- Greater Miranda

- Greenmeadow

- Leland Manor

- Old Palo Alto

- Palo Alto Orchards I Palo Alto Real Estate I Top Palo Alto Realtor

- Southgate

- University South

- Evergreen Park

- Professorville

- Ventura | Palo Alto

- Palo Alto Gardens I Palo Alto Real Estate I Top Palo Alto Realtor

- Portola Valley

- Mountain View

- Monta Loma, Mountain View

- Blossom Valley

- Castro City

- Cuernavaca

- Cuesta Park

- Jackson Park

- Martens-Carmelita

- Mountain View

- North Whisman

- Old Mountain View

- Rex Manor

- Shorline West

- The Crossings

- Whisman Station

- 175 Evandale | Mountain View Real Estate | Top Mountain View Realtor

- 2112 Wyandotte | Mountain View Real Estate | Top Mountain View Realtor

- Adobe Creek Townhouses | Mountain View Real Estate | Top Mountain View Realtor

- Aleynna Place | Mountain View Real Estate | Top Mountain View Realtor

- Alpha Villas | Mountain View Real Estate | Top Mountain View Realtor

- Americana Apartments | Mountain View Real Estate | Top Mountain View Realtor

- Appletree Lane | Mountain View | Mountain View Realtor

- Avalon Mountain View | Mountain View Real Estate | Mountain View Realtor

- Bailey's Addition | Mountain View Real Estate | Top Mountain View Realtor

- Ballentine | Mountain View Real Estate | Top Mountain View Realtor

- Baywood Park | Mountain View Real Estate | Top Mountain View Realtor

- Bedford Square | Mountain View Real Estate | Top Mountain View Realtor

- Bell Meadows | Mountain View Real Estate | Top Mountain View Realtor

- Bella Vista Acres | Mountain View Real Estate | Top Mountain View Realtor

- Bentley Square | Mountain View Real Estate | Top Mountain View Realtor

- Birchgreen | Mountain View Real Estate | Top Mountain View Realtor

- Bon View Terrace | Mountain View Real Estate | Top Mountain View Realtor

- Bonita Gardens | Mountain View Real Estate | Top Mountain View Realtor

- Boranda Ave Condominiums | Mountain View Real Estate | Top Mountain View Realtor

- Bonita Gardens | Mountain View Real Estate | Top Mountain View Realtor

- Boranda Avenue Condominiums | Mountain View Real Estate | Top Mountain View Realtor

- Borde Vista Place | Mountain View Real Estate | Top Mountain View Realtor

- Brookside Park | Mountain View Real Estate | Top Mountain View Realtor

- Bryant Square | Mountain View Real Estate | Top Mountain View Realtor

- Buena Vista | Mountain View Real Estate | Top Mountain View Realtor

- Camille Park | Mountain View Real Estate | Top Mountain View Realtor

- Caviglia Tract | Mountain View Real Estate | Top Mountain View Realtor

- Central Los Altos | Mountain View Real Estate | Top Mountain View Realtor

- Central Mountain View | Mountain View Real Estate | Top Mountain View Realtor

- Charleston Village Condominiums | Mountain View Real Estate | Top Mountain View Realtor

- Cherry Wood Acres | Mountain View Real Estate | Top Mountain View Realtor

- City Centre Homes | Mountain View Real Estate | Top Mountain View Realtor

- Classics at Evandale | Mountain View Real Estate | Top Mountain View Realtor

- Classics of Miramonte | Mountain View Real Estate | Top Mountain View Realtor

- Cloverdale | Mountain View Real Estate | Top Mountain View Realtor

- Dalma 30 | Mountain View Real Estate | Top Mountain View Realtor

- Downtown Mountain View | Mountain View Real Estate | Top Mountain View Realtor

- El Prado | Mountain View Real Estate | Top Mountain View Realtor

- Estrada Park | Mountain View Real Estate | Top Mountain View Realtor

- F.A Pritchett | Mountain View Real Estate | Top Mountain View Realtor

- Fairbrook | Mountain View Real Estate | Top Mountain View Realtor

- Fairview | Mountain View Real Estate | Top Mountain View Realtor

- Fretz Tract | Mountain View | Top Mountain View Realtor

- Garden Terrace | Mountain View Real Estate | Top Mountain View Realtor

- Garliepp | Mountain View Real Estate | Top Mountain View Realtor

- Gemello | Mountain View Real Estate | Top Mountain View Realtor

- Gest Ranch | Mountain View Real Estate | Top Mountain View Realtor

- Glumaz | Mountain View Real Estate | Top Mountain View Realtor

- Golf Course Estates | Mountain View Real Estate | Top Mountain View Realtor

- Granada Condominiums | Mountain View Real Estate | Top Mountain View Realtor

- Granada Park Townhomes | Mountain View Real Estate | Top Mountain View Realtor

- Grant Townhomes | Mountain View Real Estate | Top Mountain View Realtor

- Grove's Gardens | Mountain View Real Estate | Top Mountain View Realtor

- Hamwood | Mountain View Real Estate | Top Mountain View Realtor

- Haynes | Mountain View Real Estate | Top Mountain View Realtor

- Heatherstone Manor | Mountain View Real Estate | Top Mountain View Realtor

- Heatherstone | Mountain View Real Estate | Top Mountain View Realtor

- Hollingsworth Tract | Mountain View Real Estate | Top Mountain View Realtor

- Hollywood | Mountain View Real Estate | Top Mountain View Realtor

- Hubbard Tract | Mountain View Real Estate | Top Mountain View Realtor

- J.B. Graham | Mountain View Real Estate | Top Mountain View Realtor

- J.C. Harding Tract | Mountain View | Top Mountain View Realtor

- Lone Pine | Mountain View Real Estate | Top Mountain View Realtor

- Mardell Manor | Mountain View Real Estate | Top Mountain View Realtor

- Mariach | Mountain View Real Estate | Top Mountain View Realtor

- Mariposa Heights Condominiums | Mountain View Real Estate | Top Mountain View Realtor

- Meadow Glenn | Mountain View Real Estate | Top Mountain View Realtor

- Mechling | Mountain View Real Estate | Top Mountain View Realtor

- Miramar | Mountain View Real Estate | Top Mountain View Realtor

- Midrock | Mountain View Real Estate | Top Mountain View Realtor

- Miramar | Mountain View Real Estate | Top Mountain View Realtor

- Mockbee & Weilheimer Addition | Mountain View Real Estate | Top Mountain View Realtor

- Monroe Estates | Mountain View Real Estate | Top Mountain View Realtor

- Monta Loma | Mountain View Real Estate | Top Mountain View Realtor

- Monta Vista Circle | Mountain View Real Estate | Top Mountain View Realtor

- Montecito Pines | Mountain View Real Estate | Top Mountain View Realtor

- Moore Manor | Mountain View Real Estate | Top Mountain View Realtor

- Mountain Shadows Country Club Homes | Mountain View Real Estate | Top Mountain View Realtor

- Mountain Shadows | Mountain View Real Estate | Top Mountain View Realtor

- Mountain View Gardens | Mountain View Real Estate | Top Mountain View Realtor

- Nelson Manor | Mountain View Real Estate | Top Mountain View Realtor

- New Mill | Mountain View Real Estate | Top Mountain View Realtor

- New Mountain View | Mountain View Real Estate | Top Mountain View Realtor

- Newton Manor | Mountain View Real Estate | Top Mountain View Realtor

- North Bayshore | Mountain View Real Estate | Top Mountain View Realtor

- Oaktree Commons | Mountain View Real Estate | Top Mountain View Realtor

- Palmita Park | Mountain View Real Estate | Top Mountain View Realtor

- Pamela Terrace Condominiums | Mountain View Real Estate | Top Mountain View Realtor

- Park Place | Mountain View Real Estate | Top Mountain View Realtor

- Pastoria De Las Borregas | Mountain View Real Estate | Top Mountain View Realtor

- Plymouth Colony | Mountain View Real Estate | Top Mountain View Realtor

- Q.V Middlefield Condominiums | Mountain View Real Estate | Top Mountain View Realtor

- Rancho Estates | Mountain View Real Estate | Top Mountain View Realtor

- Reinert Tracrt | Mountain View Real Estate | Top Mountain View Realtor

- Rivendell | Mountain View Real Estate | Top Mountain View Realtor

- Rockberry Villas | Mountain View Real Estate | Top Mountain View Realtor

- Ronchi | Mountain View Real Estate | Top Mountain View Realtor

- Cupertino

- Alderbrook Estates

- Autumn Gardens

- Baywood Terrace

- Beekman Place

- Belmont

- Bianchi Terrace

- Brookdale Estates

- Campo De Lozano

- Candy Rock Mountain

- Casa De Anza

- Casa Del Sol

- The Commons

- Corte Madera Highlands

- Country Life Village

- Cupertino Center

- De Anza Verdes

- De Anza Forge Condominiums

- Deep Cliffe Estates

- Garden Gate Village

- Garden View Terrace

- Glenoaks Park Villas

- Hickory Ridge

- Homestead Villa

- Huntingdon Village

- Fairgrove

- Fairway VII

- Felton Park

- Foothill Heights Apartments

- Foothills West

- Idlewild Greens

- Inspiration Heights

- Inspiration Point Monta Vista

- James Town

- Linwood Acres

- Life Village

- Loree Estates

- Los Palmas Monte Vista

- Lynton Place

- Manita Park

- Marquette Heights

- Martinwood

- The Meadows of Cupertino

- Montebello West

- Miller Manor

- Murano

- Normandy Hills

- Oakdell Ranch

- Oak Knoll Hills

- Oak Meadows

- Park Plaza

- Pacifica

- Paradise West

- Paradise West Addition

- Pepper Tree

- Portofino

- Pringlewood

- Rancho Deep Cliff

- Rancho Del Patio

- Rainbow's End

- Rivercrest

- Russelhurst Monta Vista

- Santa Clara County Roundtree

- Seven Springs

- Silveroaks West

- Sterling Square at Civic Park

- Stelling Park

- Stellar Heights

- Stonebridge

- Springarden

- Springwood Condominiums

- The Sycamores

- Town & Country Homesites

- Triumph

- Vallco Park South

- Villa Calabazas

- Villa Pacifica

- Villa Vista

- Westlyn

- The Woods

- Woods East

- White Eagle

- Williston Park

- Yeeland Heights

- York Town

- Monta Vista

- The Forum

- Baywood

- Somerset

- Montebello

- Villa Valencia

- Northpoint

- Carolyn Gardens

- Castlewood

- Monte Vista Addition

- Glenbrook Apartment Homes

- Camarda Manor

- Colony Monta Vista

- Oak Valley

- Ridgecrest

- Steven's Canyon Villas

- Westmont Park Villas

- Monte Vista Park

- Westacres

- Greenwood Circle

- Oak Grove Manor

- Rancho Ventura

- Vallco Park North

- Three Oaks

- Mann Craft Manor

- Blossom View South

- Westridge Village

- Silver Manor

- Calvert

- Sunnyvale

- Los Gatos

- A.C. Marsh

- Adobe Manor

- Albright

- Alta Heights

- Ambassador Estates

- Auzerais Survey

- Ball Tract

- Bella Vista Court

- Belwood of Los Gatos

- Bicknell

- Big Redwood Park

- Blanchard

- Blossom Dell

- Blossom Hills

- Blossom Manor

- Blossom Meadow

- Bruce Court

- Bruce Heights

- Brunskull

- Buena Vista Heights

- Cameo Park

- Cameo Park West

- Canyon View Terrace

- Casa De Los Gatos

- Castleview Heights

- Charter Oaks

- Cherry Blossom Lane

- Chirco

- Classics at Kilmer Park

- College Terrace

- Country Club Vistas

- Courtstyle

- Crescent Hill

- Crestvue Acres

- Dave's

- Daves

- Davis & Cowell

- Downing Estates

- Downing Oak

- East Los Gatos

- Edelen District

- El Gato Rancho

- El Gato Terrace

- El Rancho Padre

- El Sombroso

- Ellen E. Short

- Englewood

- Espana Oaks

- Fairview Addition

- Fillmer

- Flintridge

- Foothill Farms

- Foothills of Los Gatos

- Glen Ridge Park

- Glen Ridge Terrace

- Glen Una

- Glen Una Meadows

- Glenridge

- Greenwood Glen

- Greenwood Heights

- Hannah Sackett's Twin Oaks

- Harris

- Hidden Hill

- Highland Oaks

- Hildebrand Addition

- Hillcrest Chalets

- Hillcrest Estates

- Hillside

- Hillvale Tract

- J.G. Follett

- Johnson's Addition

- Kenwood Acres

- Kimble Tract

- La Rinconada Knolls

- Lake Canyon

- Las Cumbres

- Laurel Mews, Los Gatos

- Loma Vista Tract

- Los Gatos Creekside Village

- Los Gatos Terrace

- Los Gatos Town Manor

- Los Gatos Uplands

- Los Gatos Village

- Los Gatos Woods

- Mariposa Court

- Massol

- McCullagh Tract

- Melody Woods

- Miles & Edelen

- Montclair Oaks

- Montezuma Hills

- Nott

- Nuevo Mundo

- Oak Hill

- Oak Park Estates

- Oakwood

- Parkside

- Penn National Tract

- Pine Vista

- Placer Oaks

- Pleasant View Heights

- Pollard Oaks

- Rainbow View

- Ramelview

- Rancho De Los Gatos Town Houses

- Redberry Hills

- Ridge Crest

- Rinconada Estates

- Rinconada Highlands

- Rinconada Hills

- Rinconada Oaks

- Rinconada Terrace

- Riva Ridge

- Robison Heights

- Robsmere Terrace

- Rolling Green

- Rose Hills

- San Benito Tract

- Santa Rosa Heights

- Serena Vista

- Sereno Foothills

- Sereno Oaks

- Shannon

- Shannon Terrace

- Siekmann

- Soquel Augmentation Rancho

- Southridge

- Spotswood Tract

- Sprenkels Bungalow Park

- Stonehedge

- Stony Brook

- Stratford Estates

- Summit Woods

- Sunny Knolls

- Surmont

- Surrey Farms

- Terreno Del Sol

- Tevis Survey

- Tobey

- Twin Creeks Estates

- Vasona Oaks

- Vasona Park

- Vasona Terrace

- Vasona Venture

- Viewfield

- Villa Del Monte

- Vineland Condominiums

- Vineyard Lots

- Vista Estates

- Vista Grande

- Vista Heights

- W.J. Parr

- Walker

- Walker Partition

- West Los Gatos

- White Oaks Village

- White Oaks Village

- Wooded View Acres

- Zeda Tract

- Campbell

- Vasona Lake Park

- Hamilton East

- Central Park

- Vizcaya

- Sunnylane Tract

- Hazelwood

- Cameo Manor

- Westmont Estates

- Campus View Tract

- Fairmeadow

- Kuehnis Estates

- Bascom Court

- Shadowbrook

- San Tomas

- Sunnyoak Meadows

- Campbell's Southwestern Addition

- Vista De Las Montanas

- Brookside Court

- San Thomas Villas

- Coral Manor

- Arroyo Seco Manor

- Husted

- Los Palos

- Westmont Park

- Hacienda Heights Townhomes

- Hyde Brothers Park

- Pruneyard Villas

- Hedegard

- Pruneyard

- San Tomas Terrace

- Burlingame Gardens

- Green Bonnet Terrace

- Ampex

- Shady Dale

- White Oaks Manor

- Morgan Park

- Hyde Residential Park

- J.H. Campbell's Addition

- Shelley Greens

- Rinconada De Los Gatos

- Winchester Villa

- Western Manor

- Sunnyside

- Pinecrest Townhomes

- Ree's Subdivision

- Rose Villas

- Pruneridge Village

- Apricot Manor

- Sandalwood Townhomes

- Union Avenue Condominiums

- Garrison Tract

- Hamilton East

- Walnut Dell

- Cameo Lane

- Cook Tract

- Brookside Addition

- Arden Homesites

- Latimer Manor

- W.F. Sigal

- Oakhaven

- Parrview

- San Tomas West

- Curtis

- Sunnyside Park

- Braly Corners

- Storm

- Hacienda

- Downtown Campbell

- Dry Creek Ranch

- Excelsior Manor

- Chateau Chambord II

- Apricot Avenue

- Campbell Gardens

- Rancho Del Prado

- Claralinda

- Pepper Tree Terrace Condominiums

- Uail Park

- Llewellyn Park

- Prestige Park

- Manchester Village

- West Willow Glen Gardens

- Lovejoy Tract

- El Solyo Tract

- Aquino Park

- Campbell Community Center

- Cherry Lane

- Ashlock Estates

- Fairlands

- Hacienda Village

- Bland Tract

- Lawndale

- Hamilton Condominiums

- Dry Creek Place

- White Oaks

- Morgan Park Townhouses

- Leigh Glen

- Shaahin Terrace

- Dahl's Addition

- McBain Tract

- South of Campbell Avenue

- Sunberry Gardens

- Shadow Woods

- San Tomas Haciendas

- Latimer Park

- Coventry Village

- Arroyo Gardens

- Vista Del Pueblo

- P.G. Keith's Addition

- Hershey

- Merrivale West

- Redwood City

- Saratoga

- Menlo Park

- San Jose

- Almaden Lake

- Almaden Meadows

- Almaden Valley

- The Almaden Villas

- Annabelle Tract

- Anne Darling

- Bascom - Forest

- Branham / Kirk

- Branham-Jarvis

- Brooktree

- California Maison

- Canoas West

- Calabazas North

- Cambrian

- Chaboya

- Cherry Lane Addition

- Cronwell Village

- Downtown

- Edenvale

- Flickinger South

- Fruitdale College

- Garden Alameda

- Guadalupe Oak Ranch

- Hensley

- Japantown

- Julian - St. James

- Lanai / Cunningham

- Little Portugal South

- Lone Hill Highlands

- Los Paseos

- Magliocco / Huff

- Makati

- McKay / Ringwood

- Montego

- Montevideo, San Jose

- Naglee Park

- Notting Hill / Royal Crest

- Overfelt

- Palm Haven

- Piedmont Hills

- Roberts / Walnut Woods

- Rose - Sartorette

- San Jose

- Santa Teresa

- Sierramont

- Sierra Vista Open Space Preserve

- Spartan/ keyes

- Stonegate East

- Sunrise Almaden

- Valley Forge

- Valley View - Reed

- Vendome

- Vinci South

- West San Jose

- Windmill Springs

- Atherton

- Belmont

- Monte Sereno

- Santa Clara

- Burlingame

- 38 Lorton Avenue

- Adrian Road Auto Row District

- Almer Condominiums

- Anza

- Anza Extension

- Anza Point

- Armsby Estate

- Bayfront

- Bayswater

- Belvedere Heights

- Beverly Terrace

- Burlingables

- Burlinghome

- Burlingame Grove

- Burlingame Heights

- Burlingame Hills

- Burlingame Manor

- Burlingame Plaza

- Burlingview Terrace

- Burlingame Villa Park

- Burlingame Park

- Burlingame Shore

- Burling Gables

- Camellia Court

- Canyon Terrace

- Carolands

- Central Rollins Road

- Corbitt Ranch

- Crockcroft Terrace

- Crystal Terrace

- De Coulon

- Easton Addition

- El Camino Real Gateway Corridor

- El Cerrito Park

- El Quanito Acres

- Floribunda Villas

- Glenwood Park

- Hillsborough Heights

- Hillsborough Knolls

- Hillsborough Oaksbridge

- Hillsborough Sunburst

- Inner Bayshore

- Kenmar Terrace

- La Strada

- Lakeview

- Mills Estates III

- Mills Garden Court

- Northern Gateway

- North Burlingame / Rollings Road

- North of Trousdale Drive

- Morrell Plaza Condominiums

- Oak Grove Condominiums

- Oak Grove Court

- Park Plaza Towers

- Parkwood Townhomes

- Polo Field

- Rick's Buri Buri Ridge

- Sandpiper West Condominiums

- Shoreline

- Skyfarm

- Skyline Manor

- Skyview Terrace

- Smithcrest Oaks

- Southern Gateway

- Tara Highlands

- Tobin Clark Estate

- Viewland Estate

- Villa Paloma

- Willborough Place

- Winchester Place

- Wisnon

- Woodgate Hills

- Lyon Hoag

- Ray Park

- Milpitas

- Morgan Hill

- Gilroy

- Fremont

- Newark

- Union City

- Aptos

- Boulder Creek

- Scotts Valley

- Capitola

- Santa Cruz

- Ocean View

- Live Oak

- Arana Gulch

- Cayuga

- Cleveland Ave

- Glen Canyon

- Beach Flats

- Grant Park

- Grandview

- Harvey West

- Love Creek

- Ladera Dr

- Beach Hill

- Central Park

- Alta Vista

- Pasatiempo

- Wrigley Plant

- Mission

- Paradise Park

- Prospect Heights

- River Street

- Twin Lakes

- Rolling Woods

- Santa Cruz Gardens

- Carbonera

- Villa Nueva

- Santa Cruz

- Sims

- Downtown

- South Of Laurel

- Woodland Heights

- Woods Cove Santa Cruz

- Half Moon Bay

- Review

- About

- Blog

- Home Style

- Eichler Homes

- Silicon Valley Eichler Homes

- Palo Alto Eichler Homes

- Sunnyvale Eichler Homes

- Los Altos Eichler Homes

- Portola Valley Eichler Homes

- Santa Clara Eichler Homes

- Foster City Eichler Homes

- Menlo Park Eichler Homes

- Burlingame Eichler Homes

- Mountain View Eichler Homes

- Sunnyvale Eichler Homes

- Cupertino Eichler Homes

- Saratoga Eichler Homes

- San Jose Eichler Homes

- San Mateo Eichler Homes

- Modern Homes

- Eichler Homes

- Contact

- Referral Network

- MORE

- Register

- Sign In

How School Boundaries Affect Sunnyvale Home Values

In Sunnyvale real estate, school boundaries are not just administrative lines. They are buyer-demand signals. For many families, the search for a Sunnyvale home starts with a school pathway. They want the right elementary school, the right middle school, the right high school district, the right com

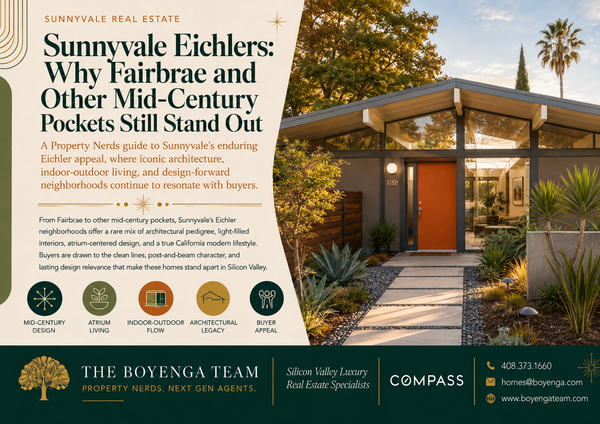

Sunnyvale Eichlers: Why Fairbrae and Other Mid-Century Pockets Still Stand Out

Sunnyvale has one of the most important Eichler stories in Silicon Valley. Palo Alto may have the bigger Eichler count. San Mateo Highlands may have the dramatic hillside mystique. San Jose’s Fairglen has historic-register recognition. But Sunnyvale has something different: the origin story, the sca

Birdland and Raynor Park: Classic Sunnyvale Neighborhoods with Big Buyer Demand

Birdland and Raynor Park are the kind of Sunnyvale neighborhoods that make Property Nerds lean forward. Not because they are flashy. Because they make sense. They sit in one of Sunnyvale’s most buyer-sensitive zones, where families, tech professionals, remodel buyers, Apple-area commuters, school-fo

Eric & Janelle Boyenga

Phone:+1(408) 373-1660